By Eric Gaus of Dodge Construction Network

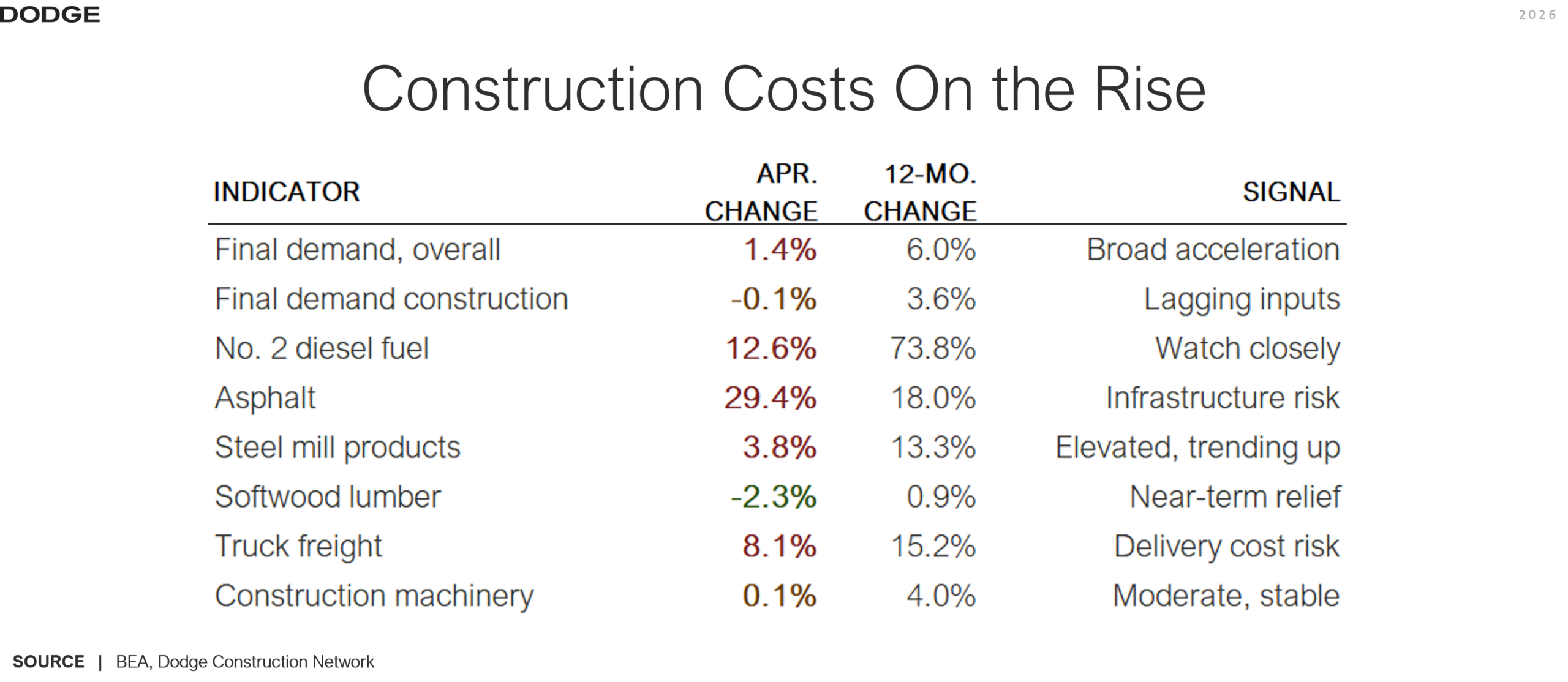

Consumer prices rose 0.6% and producer prices jumped 1.4% in April, with year over year inflation at 3.8% and 6.0%, respectively. For construction, the story is energy-driven cost escalation: diesel, gasoline, and asphalt all surged, inflating everything from equipment operation to material delivery. Final demand construction prices held relatively flat month-over-month, but the pipeline of processed goods and energy feeding job sites is running significantly hotter, putting real pressure on project margins and contract escalation terms.

April’s broad-based acceleration is not occurring in isolation. The 12-month final demand PPI of +6.0% is the highest reading since December 2022, when the post-pandemic inflation wave was at its peak. That context matters: the construction industry is now contending with a second inflationary episode in the past decade, but with a much weaker economy and labor market.

The intermediate demand pipeline, which leads final demand by weeks to months, is flashing warning signs. Prices for unprocessed goods for intermediate demand rose 4.1% in April alone and are up 20.9% over 12 months, the largest gain since September 2022. When raw and semi-processed input costs move this sharply, finished construction costs typically follow within one to two quarters. The broad-based nature of this month’s gains, touching energy, metals, chemicals, and transportation, makes a quick reversal unlikely without a significant shift in energy markets or demand conditions.

The inflation data carries meaningful implications for surety underwriters and bond professionals. With final demand construction costs up 3.6% year-over-year and input costs to construction producers running considerably hotter at 6.4%, the gap between original contract values and actual project completion costs continues to widen. For performance and payment bonds, this cost escalation raises the risk that contractors operating under fixed-price contracts are increasingly undercapitalized relative to the work remaining, a classic precursor to contractor distress and potential bond claims.

Materials-intensive trades exposed to metals inflation (steel mill products up 15.4% year-over-year, nonferrous metals up 67%) face margin compression that may not be visible in a contractor’s financials until mid-project. Surety professionals reviewing new bond submissions or monitoring existing exposure should be probing contractors on their fuel and metals escalation provisions, the adequacy of contingency allowances in their backlogs, and whether subcontractor pricing reflects current market conditions rather than those in place when bids were originally submitted.

Eric Gaus is Chief Economist at Dodge Construction Network, where he directs economic research. He brings over 15 years of experience in academia and the private sector, creating macroeconomic models and producing research on critical issues for the global economy. Prior to joining Dodge, Gaus was a Director at Moody’s, where he managed the development and maintenance of their global forecasting model and served as the product manager of their country risk service. He received his PhD from the University of Oregon and spent several years teaching at small liberal arts colleges. While in academia, Gaus published articles on the role of expectation formation in macroeconomics and finance. He can be reached at Eric.Gaus@construction.com.

Get Important Surety Industry News & Info

Keep up with the latest industry news and NASBP programs, events, and activities by subscribing to NASBP SmartBrief.