By Eric Gaus of Dodge Construction Network

As military activity in the Persian Gulf region stretches into its third week, the prospect of a significant oil price shock seems like a meaningful possibility. Being a large input to construction activity, an increase in the oil price will slow down construction, but how much and for how long? The economics team at Dodge explored two scenarios to give some sense of the impact on the construction industry and the surety business that supports it. In our worst-case scenario total construction activity is about 2% lower than our current baseline assumptions; meaningful but not catastrophic.

The situation in the Middle East is very fluid and has the potential to be very disruptive. 20% of the world’s oil flows through the Strait of Hormuz, and Iran has a stranglehold on the narrow water way. Even though almost all of the oil going through the strait heads towards Asia and Europe, oil is a global commodity and therefore we here in the US will face higher prices as well.

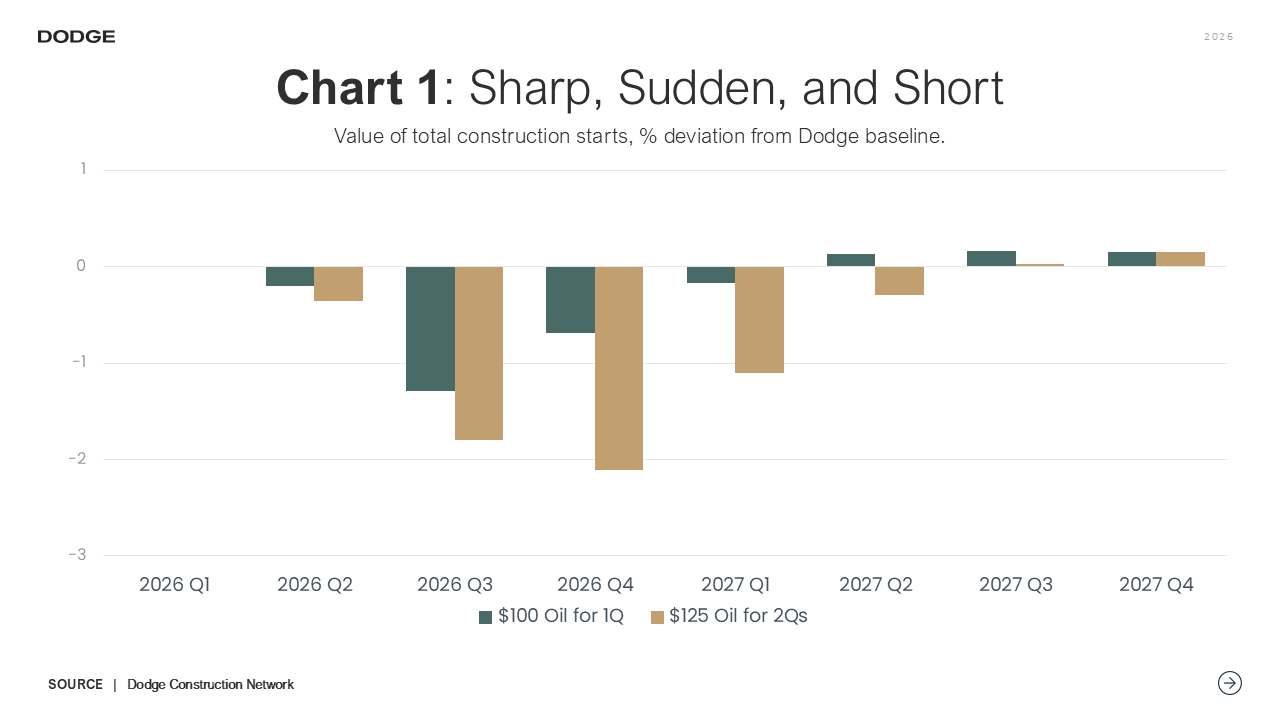

Our current baseline assumes a quick normalization of oil prices; however, each day makes that prospect less likely. We conducted two alternative scenarios to provide some window into the potential impacts of a drawn-out conflict. In the first, oil prices rise to $100 per barrel for one full quarter before slowly falling back to the $60 mark. In the second, we reach $125 for 2 full quarters.

There is a delay between the shock and the impact on construction starts, as the higher oil prices will do little to stop projects on the cusp of breaking ground. By Q3 in the first scenario and Q4 in the second scenario we feel the full impact of these extended disruptions (see Chart 1). The overall impact is between a decline in the value of total construction starts of about 1.5 to 2 percentage points lower than our current baseline.

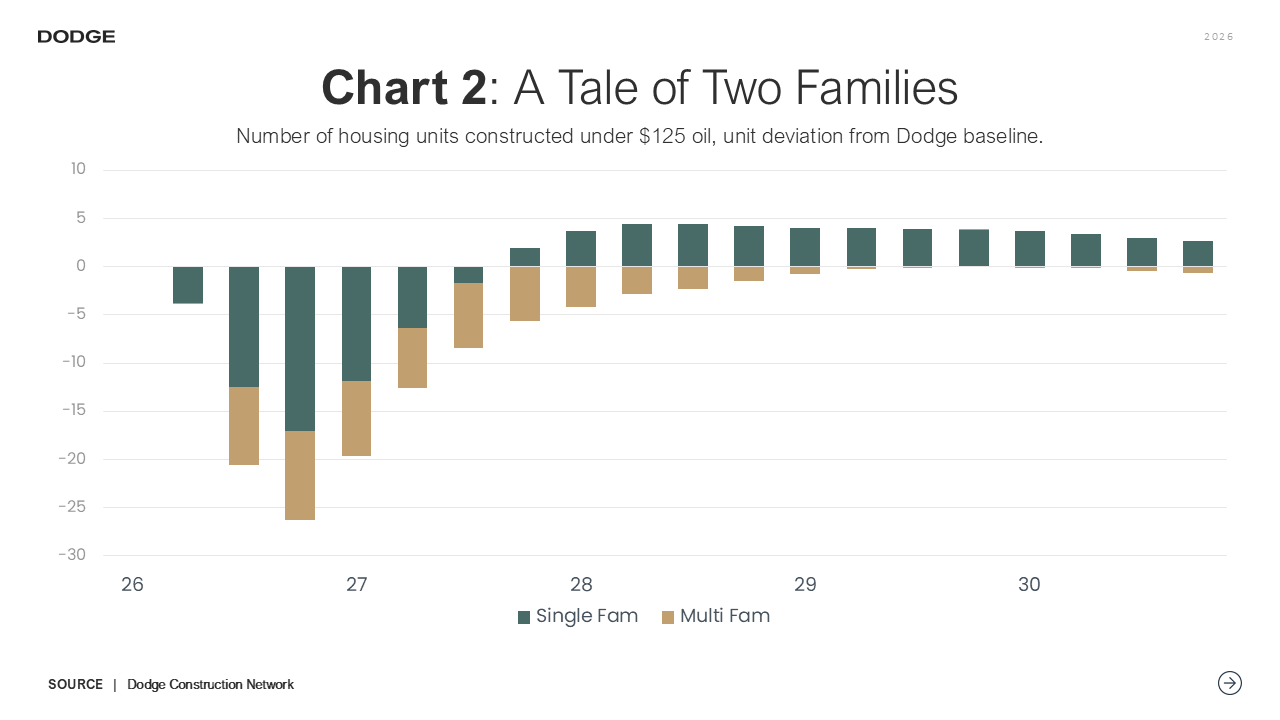

The residential vertical suffers the worst. The impact is about 100k fewer units through 2028, with the single family market responding more quickly than multifamily (see Chart 2). Commercial construction gets a delayed hit and not quite as hard as residential, only sustaining 1-1.5% declines relative to the baseline. Institutional and non-building come out largely unscathed thanks to a relatively larger proportion of government contracts and longer time horizons. Thus, surety portfolios heavier in residential and commercial will be at greater risk.

Since this is a supply side shock, there are also price effects. Construction cost inflation will increase 0.25-0.50 percentage points further stressing the surety industry. The positive news is that the damage is not so severe that one can expect a sharp increase in the number of claims, but those that do come through will likely be more costly than anticipated.

The views expressed in this article are solely those of the author and do not necessarily represent those of NASBP.

Eric Gaus is Chief Economist at Dodge Construction Network, where he directs economic research. He brings over 15 years of experience in academia and the private sector, creating macroeconomic models and producing research on critical issues for the global economy. Prior to joining Dodge, Gaus was a Director at Moody’s, where he managed the development and maintenance of their global forecasting model and served as the product manager of their country risk service. He received his PhD from the University of Oregon and spent several years teaching at small liberal arts colleges. While in academia, Gaus published articles on the role of expectation formation in macroeconomics and finance. He can be reached at Eric.Gaus@construction.com.

Eric Gaus is Chief Economist at Dodge Construction Network, where he directs economic research. He brings over 15 years of experience in academia and the private sector, creating macroeconomic models and producing research on critical issues for the global economy. Prior to joining Dodge, Gaus was a Director at Moody’s, where he managed the development and maintenance of their global forecasting model and served as the product manager of their country risk service. He received his PhD from the University of Oregon and spent several years teaching at small liberal arts colleges. While in academia, Gaus published articles on the role of expectation formation in macroeconomics and finance. He can be reached at Eric.Gaus@construction.com.

Get Important Surety Industry News & Info

Keep up with the latest industry news and NASBP programs, events, and activities by subscribing to NASBP SmartBrief.