By Eric Gaus of Dodge Construction Network

For an institution expected to be academic, stately, and placid, the Federal Reserve is looking a little jumpy. And it has good reason to be. Changes in the Fed’s perception about future policy imply higher market interest rates going forward regardless of the actual changes of policy rate. For the bond and surety market that means a higher cost of capital.

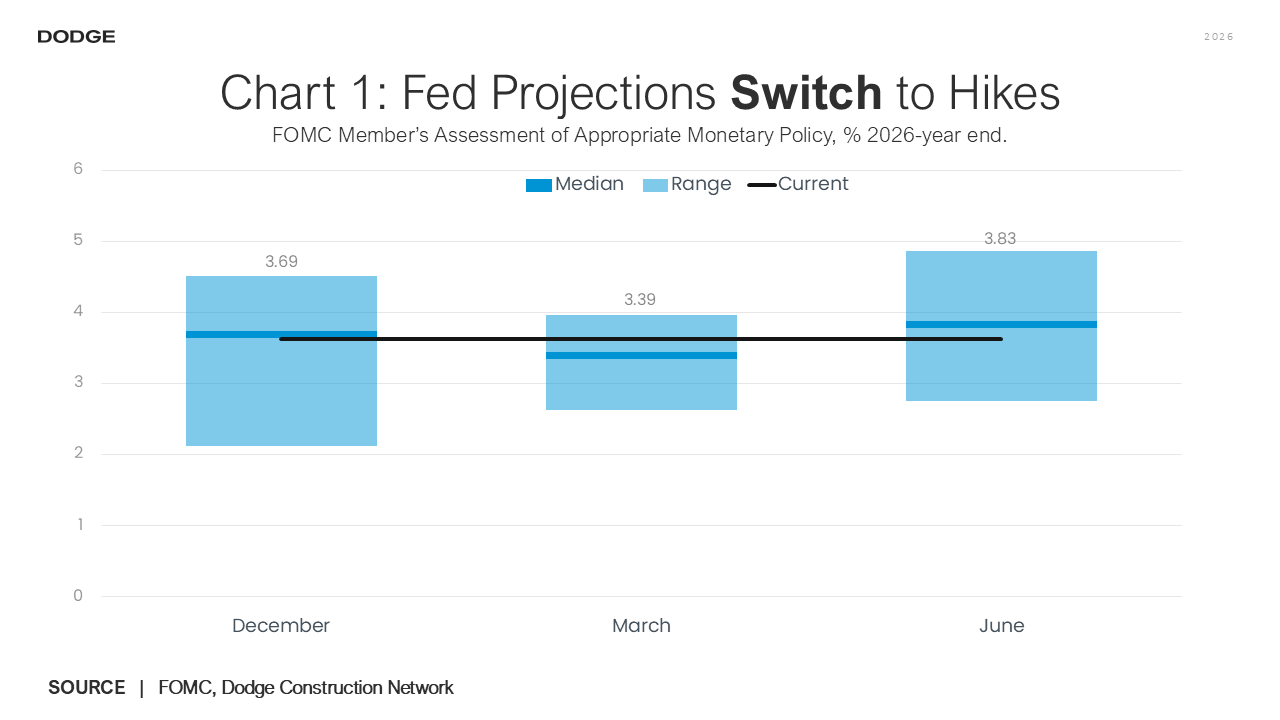

Personal consumption expenditures inflation, the key metric used by the Fed, came in at 4.1% last week. That is more than double their stated inflation target of 2 percent. In 6 months, the Fed has gone from telegraphing steady rates, to falling rates, and now a balance of raising rates (see Chart 1). This frenetic change in perception is more than personnel changes, though Chairperson Kevin Warsh will undoubtedly influence the trajectory of future policy.

We came into 2026 with a high degree of uncertainty. Indeed, the Fed’s so-called “dot-plot” was one of the widest on record, with some Federal Reserve members calling for two hikes over the year and another suggesting a full percentage point decline. The weak labor market data convinced the majority of members of the Federal Open Market Committee (FOMC) of the Federal Reserve System that lower rates were in the cards by March. But the surge of inflation following the closure of the Strait of Hormuz coupled with stronger jobs data have flipped members’ opinions of optimal policy.

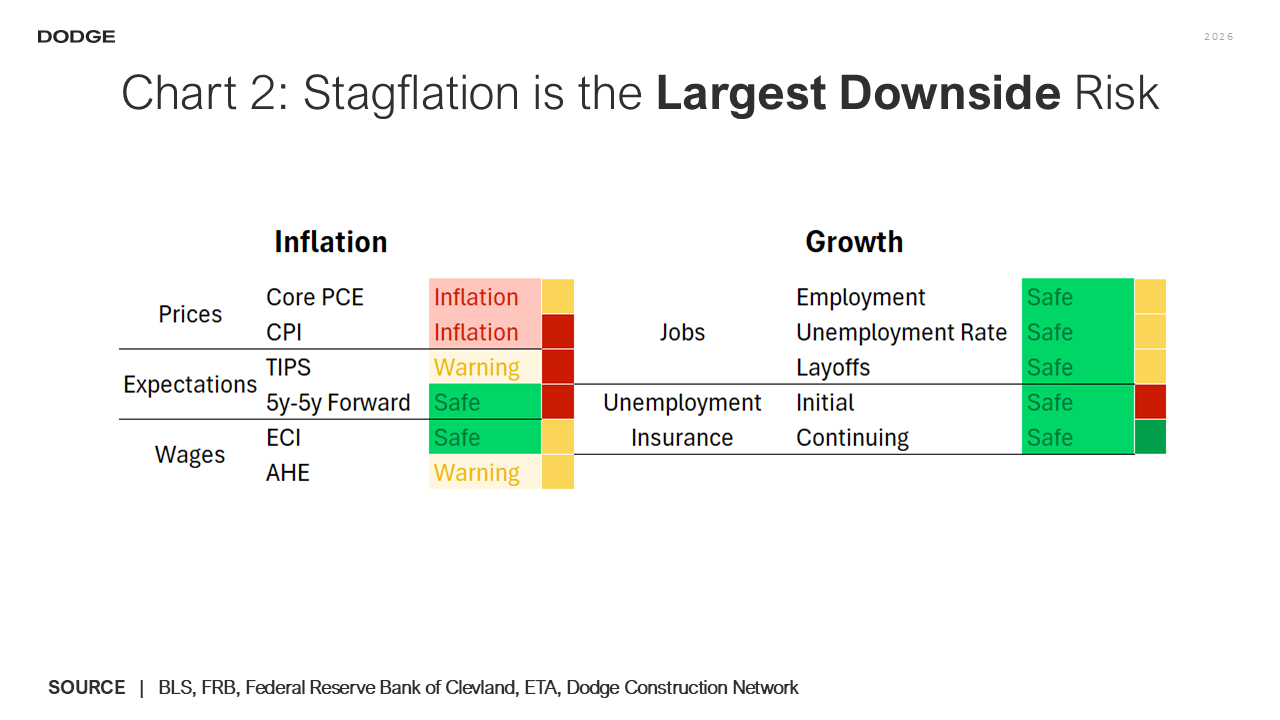

The flip-flopping of forward guidance may be a manifestation of the uncertainty felt at the beginning of the year. That is, policy decisions by the executive branch have been swift and disruptive, rapidly changing the actual and potential path of the economy. As a result, we are seeing both sides of the Fed’s dual mandate come under pressure (see Chart 2).

Volatility on this scale typically means higher risk premia for loans regardless of what the “risk-free” rate is, and we have certainly seen upward pressure on long-dated treasuries, mortgages, and commercial loans. It is becoming increasingly clear that that uncertainty is not going away, so expect rates to remain high.

The risk-free rate will almost surely increase over the second half of the year. Given Warsh’s reiteration of the Fed’s commitment to price stability and the inflation surge clearly in the data, at least one rate hike by year end is almost certain but will not make much of a difference. However, 2 or 3 hikes are not out of the realm of possibility and would have a meaningful impact on the surety industry.

Eric Gaus is Chief Economist at Dodge Construction Network, where he directs economic research. He brings over 15 years of experience in academia and the private sector, creating macroeconomic models and producing research on critical issues for the global economy. Prior to joining Dodge, Gaus was a Director at Moody’s, where he managed the development and maintenance of their global forecasting model and served as the product manager of their country risk service. He received his PhD from the University of Oregon and spent several years teaching at small liberal arts colleges. While in academia, Gaus published articles on the role of expectation formation in macroeconomics and finance. He can be reached at Eric.Gaus@construction.com.

Get Important Surety Industry News & Info

Keep up with the latest industry news and NASBP programs, events, and activities by subscribing to NASBP SmartBrief.